Understanding Scope 1, 2, and 3 emissions

06.06.2024

·

Maddalena Castelli Dezza

What are Scope 1, 2 and 3 GHG emissions?

Scope 1, 2, and 3 are a way of categorizing greenhouse gas (GHG) emissions based on their source and on the level of control an organization has over them.

These scopes, defined by the Greenhouse Gas Protocol (GHG Protocol), provide a structured method for organizations to measure and disclose their carbon footprint.

The definitions of the three scope are as follows:

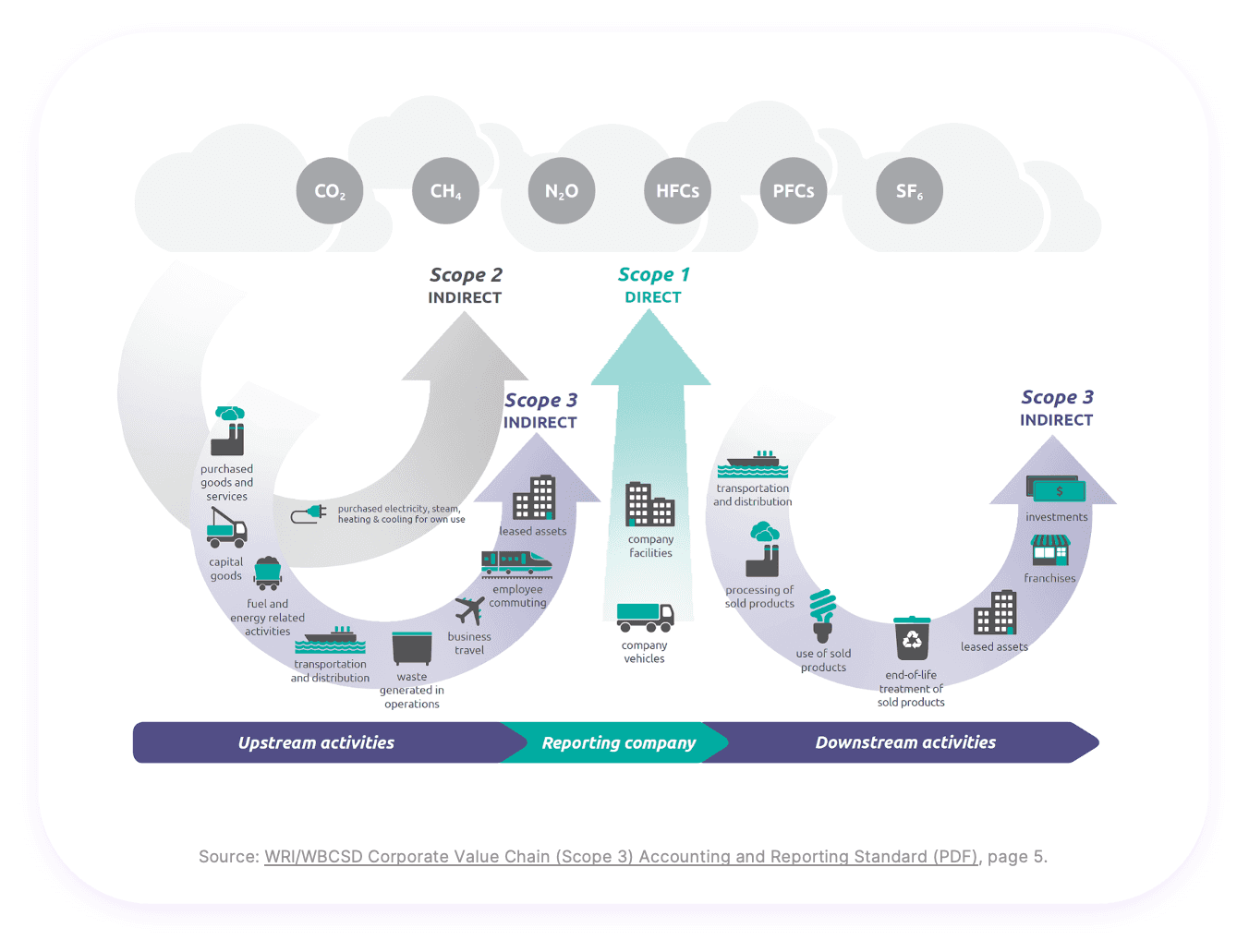

Scope 1: This includes direct greenhouse gas emissions originating from sources directly owned or controlled by the company. Examples include emissions from fuel combustion within facilities and vehicles, as well as fugitive emissions.

Scope 2: Refers to indirect GHG emissions from the generation of purchased electricity, steam, heat and cooling.

Scope 3: Extending beyond the company's immediate operations, Scope 3 captures the indirect emissions associated with its entire value chain. These emissions can occur before (upstream) or after (downstream) the company's own activities. The GHG Protocol further divides Scope 3 emissions into 15 categories.

Let's explore the three scopes in more detail:

Scope 1

Scope 1 includes emissions originating from sources directly owned or controlled by the company, making them direct emissions attributable to the company. Scope 1 emissions are further categorized into:

Stationary combustion: These emissions arise from the combustion of fuel in stationary devices such as boilers powered by natural gas, incinerators, combustion turbines.

Process emissions: Most of these emissions originate from the production or processing of chemicals and materials, such as cement, aluminum, ammonia, and waste.

Fugitive emissions: These emissions occur from the leakage of refrigerant gas from refrigeration systems like fridges and chillers, as well as air conditioning units.

Mobile combustion: This category includes emissions from mobile sources owned or controlled (leased) by the company, such as company cars, trucks, and forklifts.

Scope 2

Scope 2 covers emissions arising from the consumption of purchased electricity, steam, heat, or cooling. These emissions are categorized as indirect because they result from activities of the reporting organization but occur at sources owned or controlled by other entities.

The GHG Protocol distinguish two methods for Scope 2 accounting:

Location-based method: This method reflects the average emissions intensity of the national grids where energy consumption takes place.

Market-based method: This approach considers emissions from electricity chosen by companies. It uses emission factors provided by energy suppliers and the energy contracts selected.

Both methods are useful for different purposes. A market-based estimation shows the emissions for which the company is accountable due to its purchasing decisions, while the location-based method helps understand the impacts of operations without market influences. Employing both methodologies provides a comprehensive assessment of risks, opportunities, and changes in emissions from electricity supply.

Scope 3

Scope 3 includes all other indirect emissions which result from the company's activities but arise from sources not owned or controlled by the company. The GHG Protocol further divides Scope 3 emissions into 15 distinct categories.

Upstream emissions

1: Purchased Goods and Services: Emissions from products purchased or acquired by the company in the reporting year. Products include both goods (tangible products) and services (intangible products).

2: Capital Goods: Emissions from durable products, usually plants, equipment and properties, used by the company.

3: Fuel- and Energy-Related Activities Not Included in Scope 1 or Scope 2: Emissions related to the production of fuels and energy purchased and consumed by the reporting company in the reporting year that are not included in scope 1 or scope 2.

4: Upstream Transportation and Distribution: Emissions from the transportation of purchased products from the supplier to the reporting company, as well as third-party transportation and distribution services purchased by the reporting company in the reporting year.

5: Waste Generated in Operations: Emissions from waste disposal and treatment.

6: Business Travel: Emissions from the transportation of employees for business- related activities in vehicles owned or operated by third parties, such as aircraft, trains, buses, and passenger cars.

7: Employee Commuting: Emissions from employee transportation between home and work. It may include emissions from home working (i.e., employees working remotely)

8: Upstream Leased Assets: Emissions from leased assets operated by the company.

Downstream emissions

9: Downstream Transportation and Distribution: Emissions from product transportation after sale.

10: Processing of Sold Products: Emissions from product processing by third parties.

11: Use of Sold Products: Emissions from product use by customers.

12: End-of-Life Treatment of Sold Products: Emissions from the waste disposal and treatment of products sold at the end of their life.

13: Downstream Leased Assets: Emissions from leased assets owned by the company.

14: Franchise: Emissions from franchise operations.

15: Investments: Emissions associated with company investments.

Companies are expected to comprehensively report on Scope 3 emissions by calculating emissions for each relevant category contributing significantly to the total Scope 3 emissions and justifying any excluded categories.

In most cases, Scope 3 emissions constitute the majority of a company's greenhouse gas emissions. According to the CDP (Carbon Disclosure Project), these emissions typically are around 75% of a company's total emissions. However, the specific sources can vary significantly. For instance, in the Oil & Gas sector, the "use of sold products" makes up approximately 80% of total emissions, while emissions from investments account for nearly 100% in the financial services sector.

Tips for Scope 3 reporting

Calculating Scope 3 emissions requires more effort compared to Scope 1 and Scope 2 as it involves engaging suppliers and going deeper into the value chain. Furthermore, accessing the necessary data points can be challenging and they may be unavailable.

When direct data is lacking, organizations may use secondary data in their inventory, such as industry-average data, extended input-output data, or proxies. While this helps fill data gaps, it can also lead to decreased reporting accuracy.

Here are eight tips and resources for calculating Scope 3 emissions:

Consult the Scope 3 calculation guidance provided by the GHG Protocol, which offers the methodologies to estimate emissions across all 15 categories.

Establish methodologies to monitor emissions deriving from employee activities, including business travel and commuting. Implementing a business travel tracker tool and conducting surveys on commuting patterns are valuable resources for this purpose.

Configure your ERP system to accurately track expenditures and categorize them appropriately, simplifying the year-end data collection process.

Explore the GHG Protocol website, where you can find a list of life cycle databases.

Consult The Partnership for Carbon Accounting Financials (PCAF) framework for insights on the methodologies to account for emissions from investments (Scope 3 category 15: investments).

Engage with your suppliers proactively to obtain direct emission data from the supply chain.

Ensure that all employees recognize the importance of collecting relevant data for Scope 3 reporting.

Conduct an annual review to identify and implement improvements in data quality.

Why should an organization measure its GHG emissions?

Developing an emission inventory is a crucial step in understanding a company's carbon footprint. With an inventory in hand, it is possible to pinpoint areas with the highest emissions and identify reduction strategies.

Moreover, an increasing number of entities and countries are implementing regulations requiring emission tracking. For instance, companies subject to reporting obligations under the Corporate Sustainability Reporting Directive (CSRD) have to evaluate their carbon footprint. If you want to explore the carbon accounting requirements outlined in the CSRD, check out our article "Carbon accounting under the CSRD: what you need to know".

Lastly, reporting and disclosing emissions data demonstrates accountability and transparency to both customers and stakeholders. Nowadays, it's common for investors to request companies to disclose their carbon footprint and reduction strategies, as it has become a key factor in their investment decisions. Similarly, customers place greater importance on a company's environmental commitment, which significantly influences their purchasing decisions.